No money topic is too big or too small. Welcome to the Mouthy Money Podcast,…

Read More →

No money topic is too big or too small. Welcome to the Mouthy Money Podcast,…

Read More →

An energy shock in 2022 is a harbinger for potential investment market disappointment in 2026…

Read More →

It’s time for fellow millennials to start thinking about building an ISA bridge to beat…

There’s a lie many of us tell ourselves about pensions and we don’t want to…

Read More →

First-time buyers are finally reaping the benefits of higher wages and stagnant property prices in…

Read More →

Advertisement Cryptoassets have become a familiar topic in recent years, often discussed in the news…

Read More →

Advertisement Coinbase is one of the largest global platforms for trading cryptoassets. In partnership with…

Read More →

The Bank of England is duty bound to consider and prepare for exogenous shocks to…

Read More →

With 1.8 million homeowners set to remortgage in 2026, the odds of getting better rates…

Read More →

New limits on cash ISA allowances will push higher volume savers into putting more cash…

Read More →

‘Fat Cat Day’ which falls every year in early January, returned on 6 January this…

Read More →

The escalating war in Iran has driven oil prices to the highest level since 2022. That was not a good year for investors. Are we set for a repeat in 2026?

A sustained burst of inflation is the big fear. Markets have already moved swiftly to price out interest rate cuts. The Bank of England, having been expected to lop 50 basis points off the bank rate this year, is now seen as more likely to hike.

The two-year gilt yield has reacted accordingly, surging to 4.10% from 3.52% pre-conflict. The 10-year gilt yield has raced to 4.79%, up almost 60 basis points.

The US has fared slightly better. The US Dollar Index – having spent much of the last 12 months weakening, to the chagrin of non-dollar investors in US assets – is now trading over 100, having notched two consecutive weekly gains. Its strength amid fading expectations for rate cuts helps explain why gold, among the safe havens that have disappointed this crisis, has been such a damp squib.

That’s not to say all US assets have escaped unscathed. Treasury bonds across the curve have sold off since the war broke out, albeit to less dramatic degrees than the UK. The equity market has been relatively resilient.

The S&P 500 has fallen around 3% during the crisis, a surprisingly muted reaction given the lack of visibility over the duration of the supply disruption, one of the largest in the history of the oil market.

Strong corporate earnings and a robust US economy are said to explain the sanguine response. Yet revised figures last week revealed that the US economy grew at an annualised rate of just 0.7% in the fourth quarter of 2025, half the initial estimate.

Yes, the US Government shutdown was a significant drag. But a strong rebound this quarter may be tempered by a slowdown in consumer spending, a trend unlikely to be helped by higher pump prices.

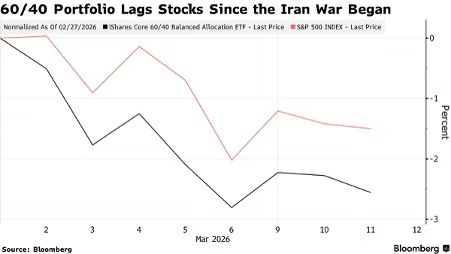

With stocks and bonds both down – and central banks facing the spectre of stagflation, their worst-case scenario – investors in balanced portfolios could again face a painful year.

In 2022, stocks and bonds famously moved in lockstep, with one key measure of correlation between those asset classes hitting 0.92 (with +1 indicating a perfect positive correlation). Today, that measure is even higher.[1]

How bad things get from here is contingent on how long the disruption persists. Iran’s Supreme Leader Mojtaba Khamenei says he wants to keep the Strait of Hormuz closed.

US strikes on military sites on Kharg Island, Iran’s vital oil export hub, have not eased tensions. Analysts at JPMorgan say a strike on Kharg’s oil sites “would immediately halt the bulk of Iran’s crude exports, likely triggering severe retaliation in the Strait of Hormuz or against regional energy infrastructure”.

If major damage is inflicted on that infrastructure, it will increase the duration of the spikes in oil and gas prices, resulting in higher global inflation.

The glass-half-full argument is that there are key differences between now and 2022. US interest rates were near zero in March that year, when US CPI was 8.6% (and Brent Crude traded above $125).

Today, the Fed’s policy rate is 3.5%-3.75% and US CPI is 2.4%. Though US markets have scrubbed out interest rate cuts – now not expected until late 2026 at the earliest – long-term inflation expectations remain sub-3%. Yields are far higher than they were in 2022. Covid, unlike then, is a distance memory.

Even so, the conflict has disrupted some of the trades that had been working well earlier in the year. Many investors had positioned for a weaker dollar and stronger emerging markets. The dollar’s sudden rebound has complicated those bets, particularly as rising energy import costs place additional pressure on developing economies, now essentially unable to cut interest rates.

Meanwhile markets like South Korea, home to chip juggernauts Samsung and SK Hynix, have had wild rides, with the KOSPI plummeting 12% in one day in early March, its biggest drop in history.

It could get much worse. With traditional safe havens offering limited protection, strategists have floated an array of alternatives, ranging from Chinese equities to uranium.

Asset managers like Invesco argue investors should hedge risk by increasing exposure not only to oil and gas, but to other commodities transported through the Strait of Hormuz, like aluminium and grains. Yet portfolio managers with less flexible mandates say there is little they can do, beyond reducing risk and waiting for greater clarity.

Geopolitical shocks can quickly fade, and stock markets have delivered positive years after major conflicts.

But if energy prices spike higher or remain elevated for months rather than weeks, this crisis may again emphasise the lesson learned in 2022: higher inflation means traditional portfolio diversification offers less protection than investors expect.

[1] https://www.longtermtrends.com/stocks-vs-bonds/#:~:text=Current%20Data,over%20the%20trailing%2012%20months