No money topic is too big or too small. Welcome to the Mouthy Money Podcast,…

Read More →

No money topic is too big or too small. Welcome to the Mouthy Money Podcast,…

Read More →

An energy shock in 2022 is a harbinger for potential investment market disappointment in 2026…

Read More →

It’s time for fellow millennials to start thinking about building an ISA bridge to beat…

There’s a lie many of us tell ourselves about pensions and we don’t want to…

Read More →

First-time buyers are finally reaping the benefits of higher wages and stagnant property prices in…

Read More →

Advertisement Cryptoassets have become a familiar topic in recent years, often discussed in the news…

Read More →

Advertisement Coinbase is one of the largest global platforms for trading cryptoassets. In partnership with…

Read More →

The Bank of England is duty bound to consider and prepare for exogenous shocks to…

Read More →

With 1.8 million homeowners set to remortgage in 2026, the odds of getting better rates…

Read More →

New limits on cash ISA allowances will push higher volume savers into putting more cash…

Read More →

‘Fat Cat Day’ which falls every year in early January, returned on 6 January this…

Read More →

For many aspiring homeowners, getting on the housing ladder has felt increasingly difficult in recent years.

Years of rapid house price growth, followed by higher mortgage rates, have stretched affordability to the limit, leaving many first-time buyers (FTBs) wondering when – or even if – they will be able to buy their first home.

But falling mortgage rates, stagnant house prices and supportive regulation have given would-be buyers fresh hope.

These seven charts show how the tide may finally be turning for those looking to take their first step onto the housing ladder.

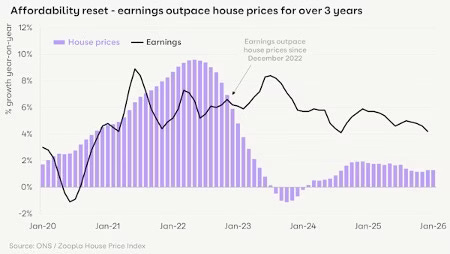

There’s been an affordability reset (of sorts)…

Stagnant house prices, rising wages and falling mortgage rates have led to an ‘affordability reset’ for first-time buyers, says Zoopla.

House prices have slowed significantly since the Bank of England started increasing interest rates in 2022, with prices growing at an annual rate of less than 2% for much of the past two years.

Wages, on the other hand, have grown much faster. Data from the Office for National Statistics shows earnings have risen by at least 4% a year – and often significantly more – for the past five years.

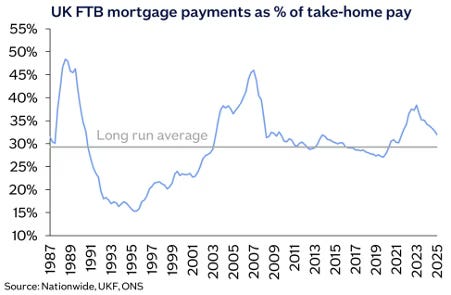

…which means financing a first home has become less of a financial burden…

Lenders have also become more willing to lend to borrowers with smaller deposits, who are seen as a riskier bet due to their limited equity. This means they are more likely to fall into negative equity – where they owe more than their property is worth – if house prices fall.

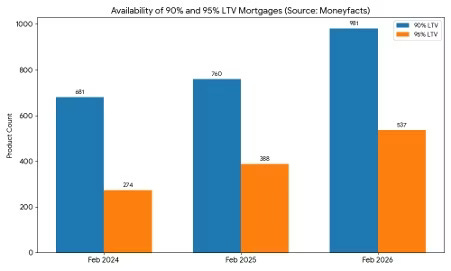

According to Moneyfacts, this shift has been dramatic. In the two years to February 2026, the number of mortgages available to borrowers with a 5% deposit (95% LTV) has surged by 96%, while products for those with a 10% deposit (90% LTV) have risen by 44%.

Government support has also played a role in increasing the availability of small deposit mortgages. The Government’s decision to continue covering part of lender losses on 95% LTV lending through the Freedom to Buy scheme has given lenders greater confidence to expand high-LTV lending.

However, there is an important caveat. Recent events in the Middle East have prompted lenders to pull large parts of their product ranges, including those designed for borrowers with small deposits.

Data from Moneyfacts shows that in the 48 hours to 11 March, lenders withdrew 472 residential mortgage products – around 6.5% of products on the market.

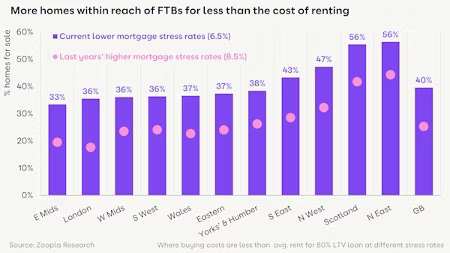

…which combined with rule tweaks has brought more properties within reach of FTBs…

The Financial Conduct Authority’s decision to clarify its guidance on mortgage stress testing in 2025 has made it easier for FTBs to qualify for a loan.

In March last year, the regulator reminded lenders of the flexibility in its affordability rules, warning some were “unnecessarily restricting access to otherwise affordable mortgages” by applying overly strict stress tests. Many had been using a ‘standard variable rate plus 1%’ approach.

The updated guidance encourages a more tailored, risk-based approach. Several major high-street lenders have since adjusted their stress tests, allowing some borrowers to access up to £40,000 more in borrowing.

In practice, most borrowers are now stress-tested at around 6.5%, compared with roughly 8.5% before the regulator clarified its position.

Savills estimated last year that the change alone could boost first-time buyer transactions by up to 24% over the next five years.

The FCA’s ongoing mortgage rule review is also expected to lead to the regulator revising its responsible lending rules to support wider access to home ownership.

… all of which has led to FTBs coming to dominate the purchase market…

Taken together, these factors mean first-time buyers are now the dominant force in the purchase market, accounting for nearly 55% of all transactions.

However, this is due as much – if not more – to do with the fact that fewer people are moving home as it is to improved conditions for FTBs.

… although – as ever with the housing market – things aren’t all plain sailing…

While conditions have improved, first-time buyers are not having it all their own way. Many parts of the UK remain unaffordable.

From a statistical perspective, an ‘affordable’ home is typically defined as costing no more than five times income. The UK average currently stands at 5.6, although it has been trending down.

National figures also mask large regional differences. In Scotland, the average home costs around four times earnings, compared with 8.8 in London, according to Nationwide.

Geopolitics has also clouded the outlook. The conflict involving Iran has pushed up swap rates – a key driver of fixed-rate mortgage pricing – prompting lenders to raise rates.

Fears the conflict could push up inflation, particularly through higher energy prices, have also led some to warn the Bank of England may need to keep rates higher for longer. However, many experts believe swap rates should ease again if the conflict proves short-lived.

In short, while conditions are improving for first-time buyers, sizeable headwinds remain.

Mortgage rates should ease if tensions involving Iran subside and swap markets settle. But a more lasting improvement will require a bigger increase in housing supply.

On that front, progress has been limited, with housebuilding still falling well short of demand. Until building accelerates, it’s hard to see any game-changing improvement in affordability.